GenVita

Connecting insurance & digital lifestyle

01/ Summary

Client

Generali

What I did

Product designer

Context

6 months – 2021

_Client Brief

Generali aspires to create a paradigm shift within the insurance sector, radically changing perceptions and expanding its reach globally.

We teamed up with the brand to complete two missions within a short timeframe: a deep-dive into why a super-app must exist to meet its objectives, and localising the experience while maintaining consistency and safeguarding Generali’s global branding.

02/ Discovery

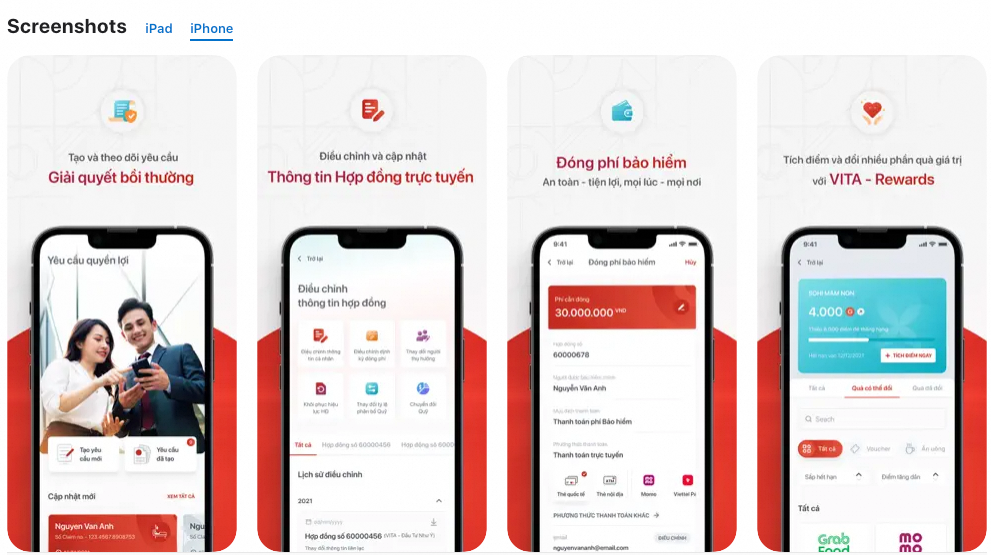

The current Genvita flow has multiple usability issues, does not cater to inexperienced of both new user and exists customers , and the UI design is outdated across all platforms and devices.

Stakeholder interview

I understand this application is not just about the end users, I need to listen and help stakeholder too. To kick start the research process, we conducted Stakeholder Interviews.

The main objectives of these interviews were to:

- Understanding the vision and expectations of our stakeholders for the brand new

- Understand the current challenges and opportunities of the GenVita app that we should dig deeper on in the research process

Round of interview

This stakeholder interviews to fully capture the project goals and objectives. These sessions were done in focus groups where stakeholders can freely share with us business and user insights.

Through stakeholder interviews, we captured the current challenges and the opportunities to improve the app.

CURRENT CHALLENGES

Basic app. There is not a lot of things users can do other than simple activities.

- Overwhelming structure of content. It was mentioned that the app does not have an intuitive structure to its content.

- Unconsolidated accounts. Lacking linkage of multiple accounts, giving difficulties for users to manage multiple accounts, which also affects Generali’s way of managing these accounts.

- Lacking “Forgot Username” journey. For those that do not remember their account details, there is not way for them to link to Zalo or Google to recover their account.

Uninformed error messages. Unhappy journeys of the app were expressed to be uninformative, leaving users hanging.

Several usability issues that can be tackled through this revamp:

- The application limits the time in payment and information editing from 7AM to 8PM

- Insurance information editing is buggy which leads to the system not updating the changes. The system didn’t update the details which have been changed from customers.

- OTP capabilities are inconsistent. The messages code in slow, and is lacking auto-populate features.

- System freezes when users make a payment.

- Upload file feature is buggy – does not process files that stated to be suitable.

OPPORTUNITIES

- Tackling current issues. Ensuring we solve the pain points and challenges, and providing a seamless experience in managing accounts.

- Easy onboarding. A quick and easy onboarding experience to drive acquisition.

- Longevity design. Ensuring that our app is capable for future additions and development.

- Expanding to employee insurance. Users are not able to find any company insurance policy information on the app.

- Gifts module. The current gift section is basic (lacking features such as sort, filters, etc) and could be extended more into something more valuable.

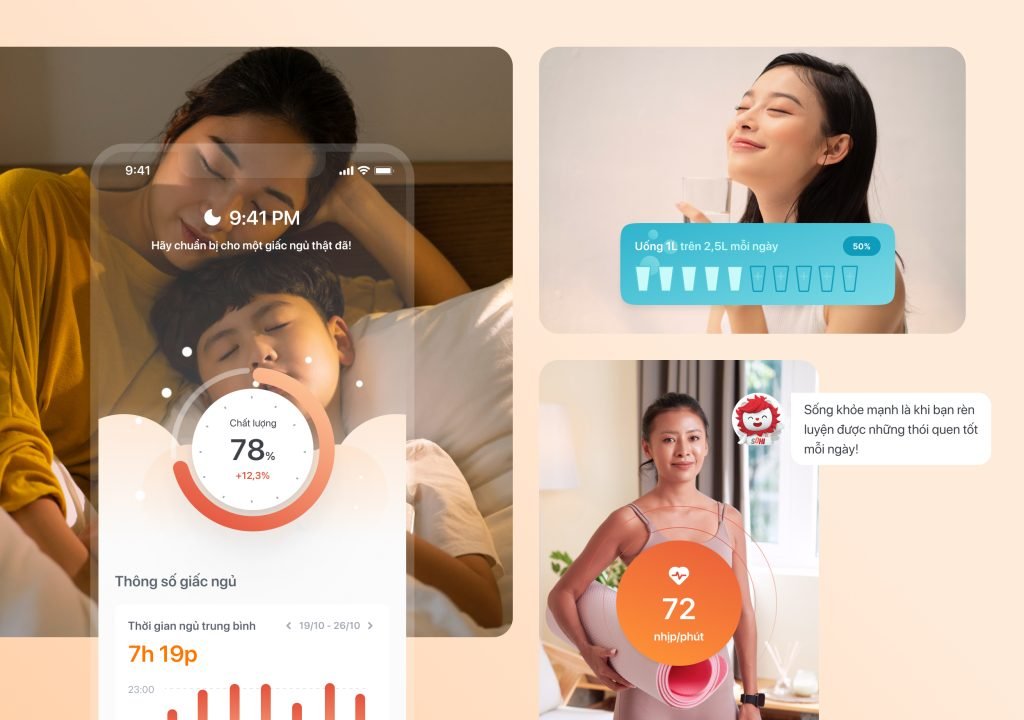

- Extended telemedicine features. With the uprising trend of telemedicine, the current app lacks the capability to connect with a doctor through voice/video call

- Increase awareness. A tool to build brand identity and help attract potential customers.

- Lifestyle integration. Being a part of customers lives outside of insurance needs. Looking into health features to create habits within our users. Al assistants to remind users on certain actions on information.

- Understanding our customers. Through daily engagement, we can uncover distinct trends and behaviour shifts in our customer data. This could help us understand their needs

- Smart nudging. Providing a space to upsell/cross sell Generali products and services without being too intrusive.

- Seamless web and app experience. Ensuring experience is delivered consistently on web and mobile.

Landscape analysis

To innovate, we must first understand the current landscape of digital insurance locally and globally.

I can do this through a landscape analysis, where we can identify key gaps and opportunities that can leverage on between our digital products and the competitors’.

This provides strategic insights into the features, functions, flows, and feelings evoked by the design solutions of our competitors.

By understanding these facets of competitors’ products, can strategically design our solution with the goal of making a superior experience

Local competitions

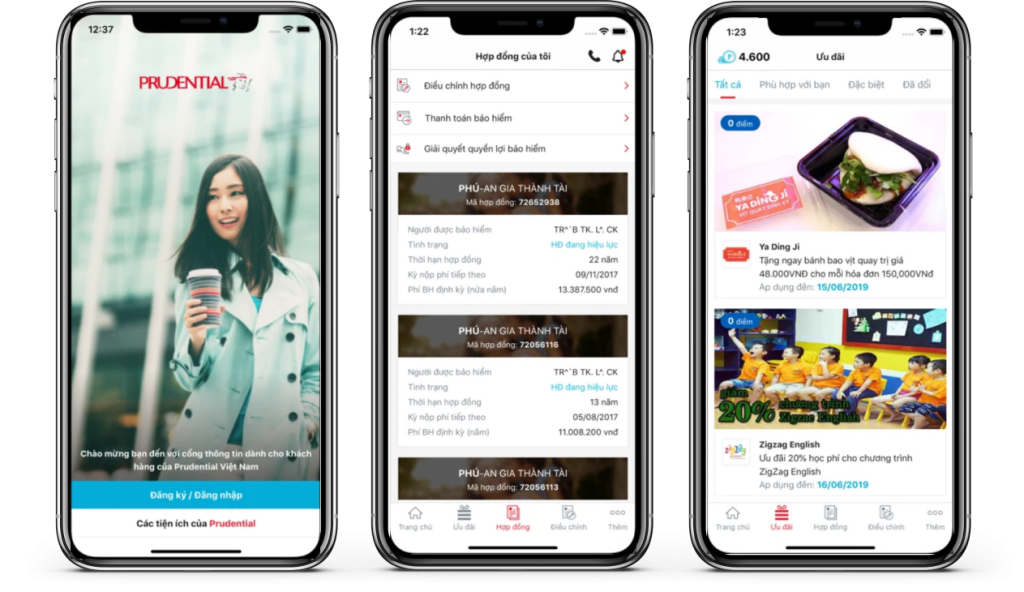

1/ PRUoline – Prudential Vietnam

- Managing contract. Manage easily the status of your Life Insurance policy anytime, anywhere with simple clicks.

- Paying Insurance fee. Fast, secure online Premium Payments for one or more policies at the same time

- Rewards. Allows customers to register for PRUrewards app – this is the first Prudential Loyalty Program where customers are given the right to actively choose gifts and incentives.

- Modifying contract. Easily change contact information for one or more contracts at the same time.

- Claim process. Send quickly the insurance documents of claim case via this app

OPPORTUNITIES – A well-executed loyalty/reward system could easily increase engagement on the app.

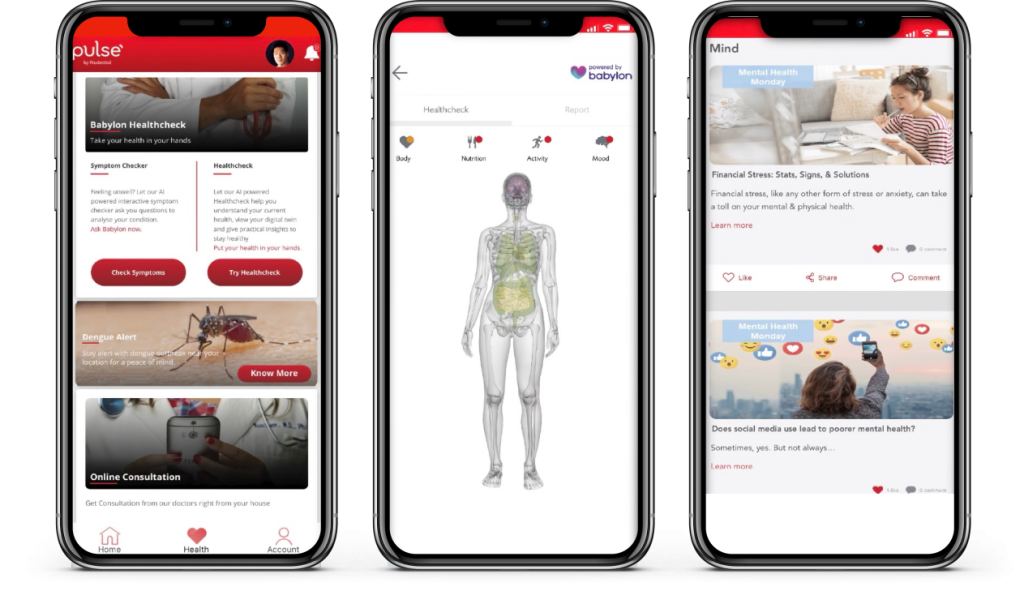

2/ We do pulse

- Heath Checker. Complete an online assessment and. get insights to your health through “Digital Twin”.

- Symptom Checker. Understand your symptoms better and learn about potential causes, conditions, and issues with easy-to-understand information when you answer a series of questions.

- Telemedicine. Get easy access to medical healthcare on the go.

- Hospitals and Clinics Locator. Find a nearby Clinic and Hospital.

- Tracking your progress with a fitness tracker. Imports health data from existing heath apps and wearable.

- Health Channels: Check out health & lifestyle articles.

OPPORTUNITIES – Prudential took a step further in their telemedicine services and offer extensive telemedicine features. There is an opportunity for us to learn from their features and integrate it in our current app, providing a one-stop experience.

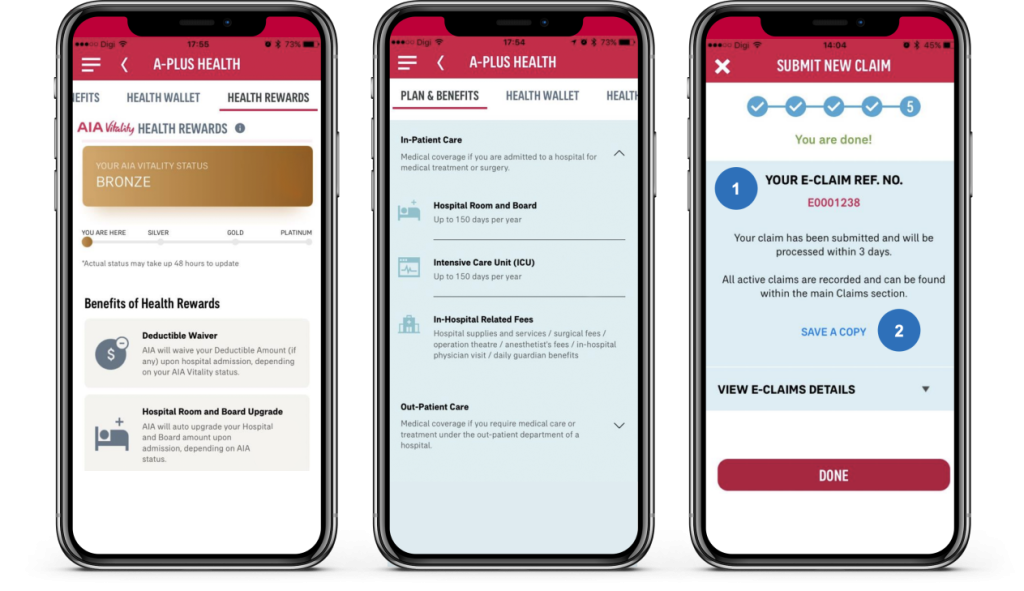

3/ My AIA

- AIA Vitality. By Personalising and tracking your exercising plan. Set weekly and daily goals and earn rewards for the healthy habits.

- Financial Health Check. Search the sufficiency of customer’s protection coverage by taking an assessment.

- Tele-Medicine. Chat with a doctor online, check symptom, medication deliver, list authorised doctor.

- Manage Your Medical Benefits. Cashless medical care, pre-register visit, push notification, update on insurance and medical claim online.

OPPORTUNITIES – Connecting offline and online experiences, and encourage users to live a healthy lifestyle by integrating challenges that rewards them if accomplished. Telemedicine and online diagnosis features could also be an opportunity for us especially in this pandemic era.

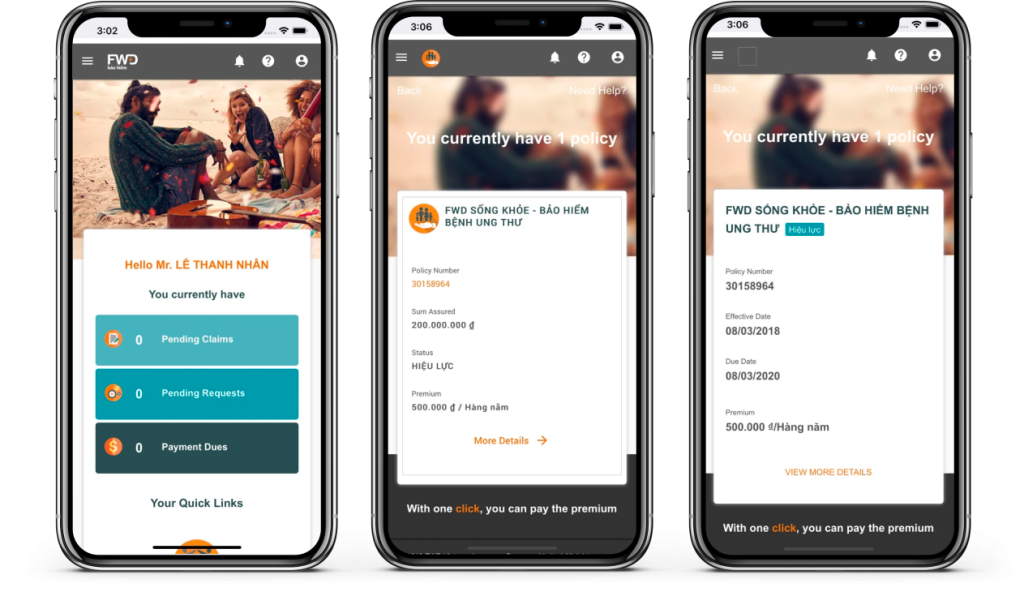

4/ FWD

- Access to insurance policies 24/7. Users can access their policy information, or other policies right from their fingertips.

- File benefit claim online. Users are able to file claims on the app.

- Online premium payment & withdrawals. Users have the ability to manage their payments and withdrawals from the app.

- Usable at best. This app only covers “hygiene” features, and does not have any interesting lifestyle elements integrated to it. This could limit engagement levels within the app.

OPPORTUNITIES – Ensuring that we provide a complete and seamless experience around the “hygiene” features of the app.

Global Industry Standards

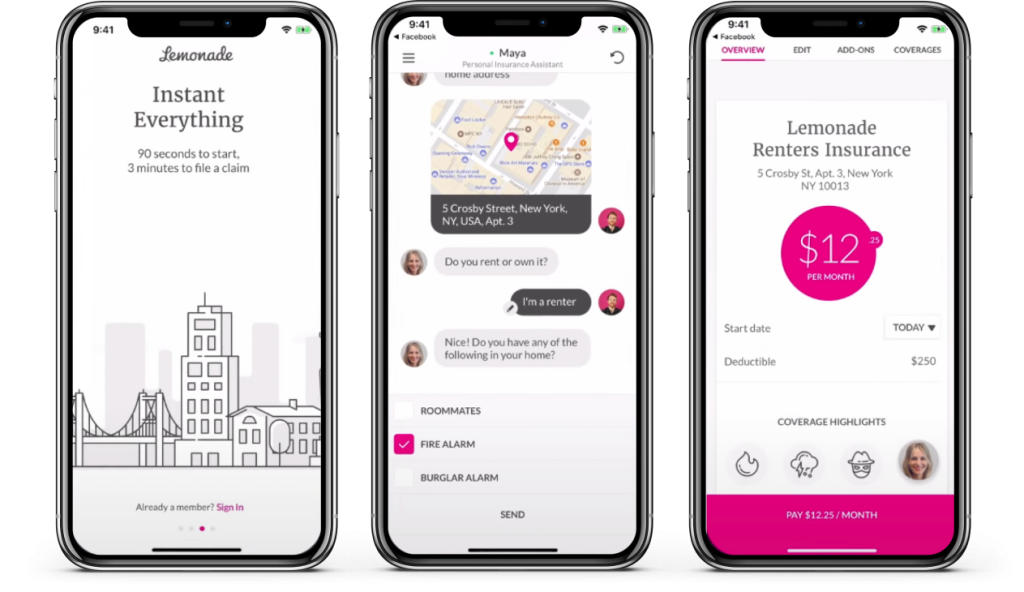

1/ Lemonade insurance

- Simplified, easy application process. Users can get a personalised policy within 90 seconds, after finishing a minor questionnaire about their personal details with an AI powered chatbot.

- Flexible coverage. Users can customise and adjust their coverage according to their preferences, giving them control of their finances. Coverages also include renters and pet insurance.

- Instant digital settlement. Claim filing can be done entirely through the app, form-free. Users only need to send a list of their claimable goods with a video detailing the incident.

- Lemonade encourages social responsibility by donating any remaining funds after claims to customers’ favourite charities.

OPPORTUNITIES – A quick and easy onboarding process can reduce drop off rates and potentially increase acquisition.

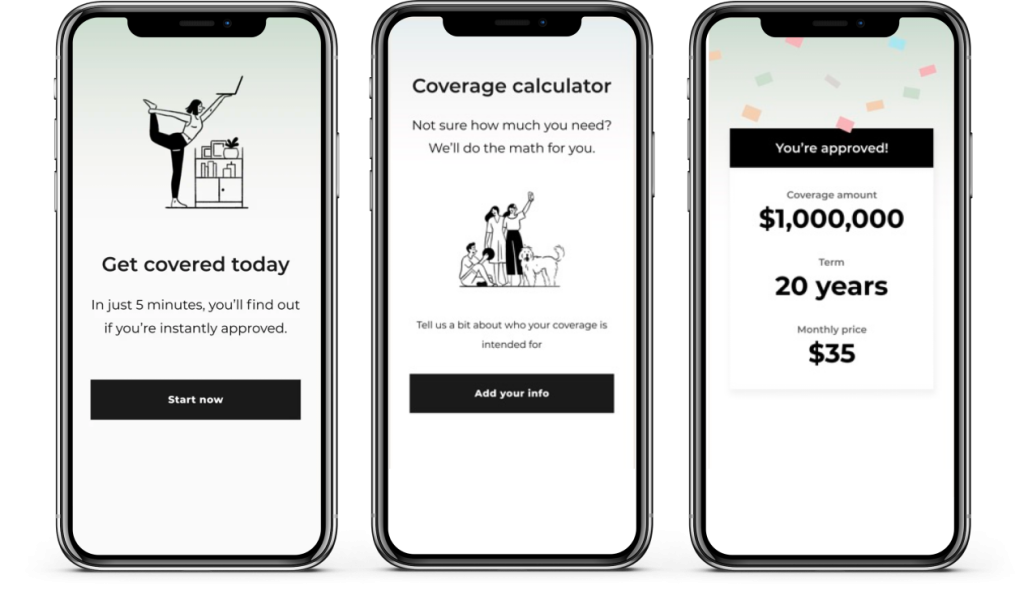

2/ Ladder – term life insurance

- Ladder promotes a streamlined experience, with policies sold and managed online without the use of agents, and instant coverage decisions that allow some customers to get insured minutes after applying.

- Ladder’s platform is cleanly designed (web and mobile), with an online quote process that gives you a quick cost estimate within a few clicks.

- These platforms also offer a guide to life insurance basics as well as a calculator to help you figure out how much coverage you need.

OPPORTUNITIES – Providing users with appropriate insurance information will help educate them and aid them in making a more informed decision when purchasing a policy.

One stop platform

1/ Wechat

- Multi-purpose app that incorporate messaging and social media features along with e-commerce, payment facilities (bank card linkage) and many more day-to-day services.

- Direct bank card linkage through WeChat Pay and e-wallet feature which permits the payment for various services within WeChat.

- Small applications within WeChat called Mini Programs that offer myriad services from purchasing goods to matchmaking.

- WeChat analytic platform to study about the traffics of Mini Programs as well as Official Accounts.

- Offering wide range (health, auto, life and travel spaces) of user-centric insurance products through WeSure, a WeChat integrated insurance platform, which form partnership with insurance providers such as Taking, Pacific Insurance, PICC, Ping An, MetLife and more.

OPPORTUNITIES – We can explore partnership strategies and understand how it can be implemented in the app. Always think : what’s in it for them?

2/ Alipay

- A third party mobile and online payment platform that supports a plethora of services and features that touches every aspects of users lives.

- Bank card linkage and e-wallet feature for the payment of various services integrated within Alipay ecosystem.

- Mini applications or programs within Alipay ecosystem offers various services from purchasing goods to booking different types of transportation.

- Users can shop through the app’s integration with Taobao, the world biggest e-commerce site that facilitate C2C retail, and Tmall, a Chinese language website that support B2C online retail.

- Health, travel, automobile and financial insurance support are available through “An Insurance Services”, an in-app Alipay feature under the partnership with big insurers like Taking Life Insurance Co.,Ping An Insurance and more.

User research

I further dove deeper to understand more about our users through desk research and user interviews.

- Understand users perceptions and preferences when it comes to insurance.

- Understand how customers currently experience the GenVita application.

- Uncover opportunities for the GenVita application revamp.

Rounds of Interviews

Real-time moderated interviews were performed online. Participants use their own desktop to answer our questions, moderators are able to communicate directly with respondents all while observing their reactions.

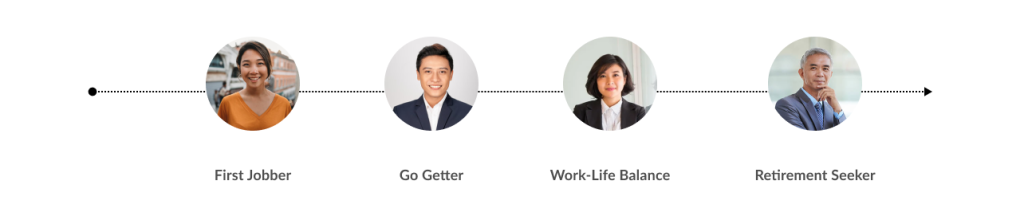

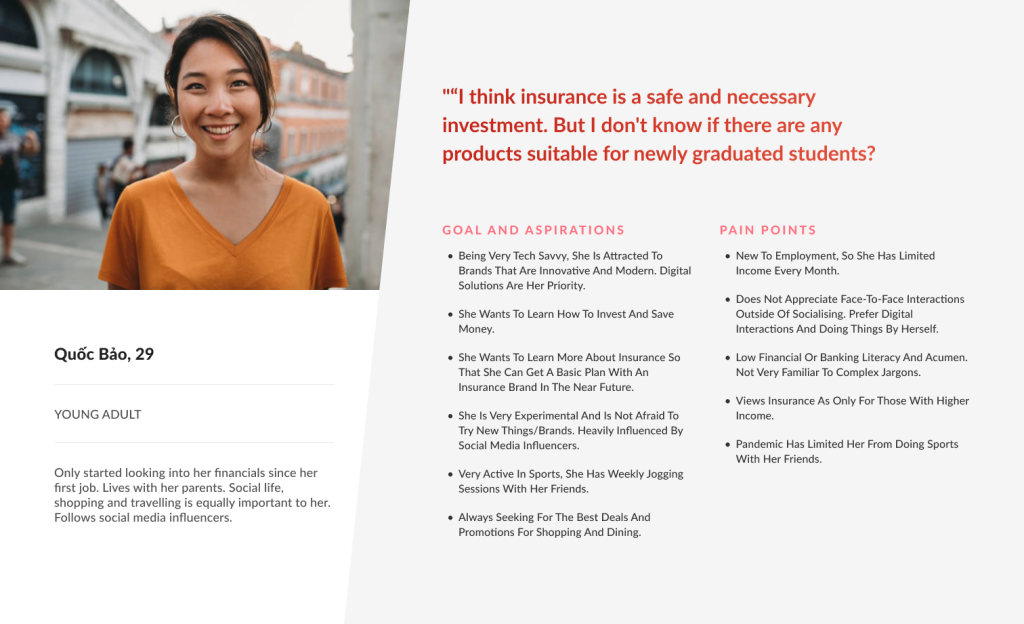

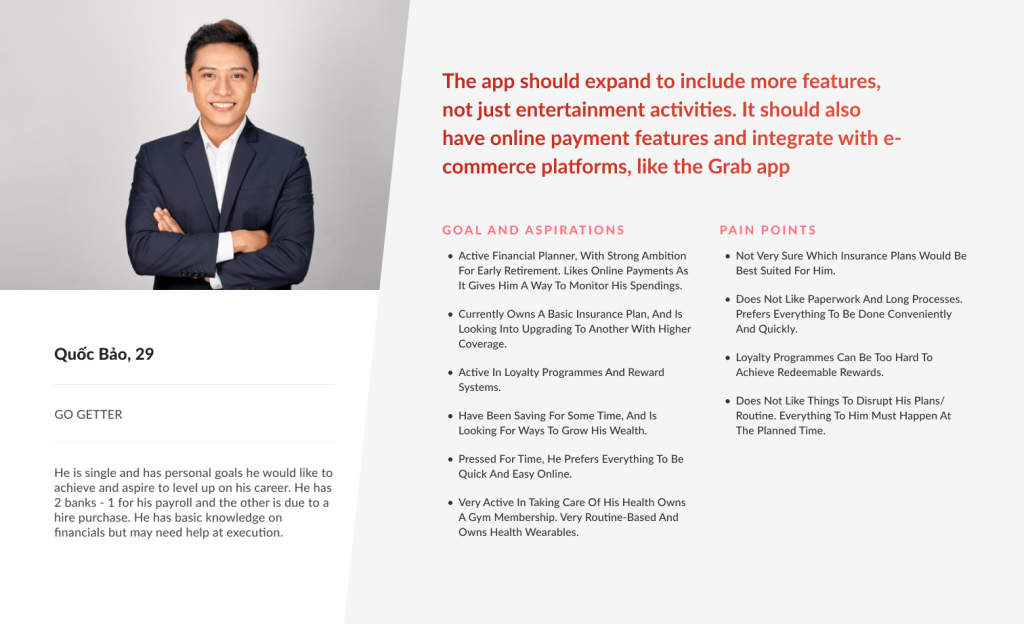

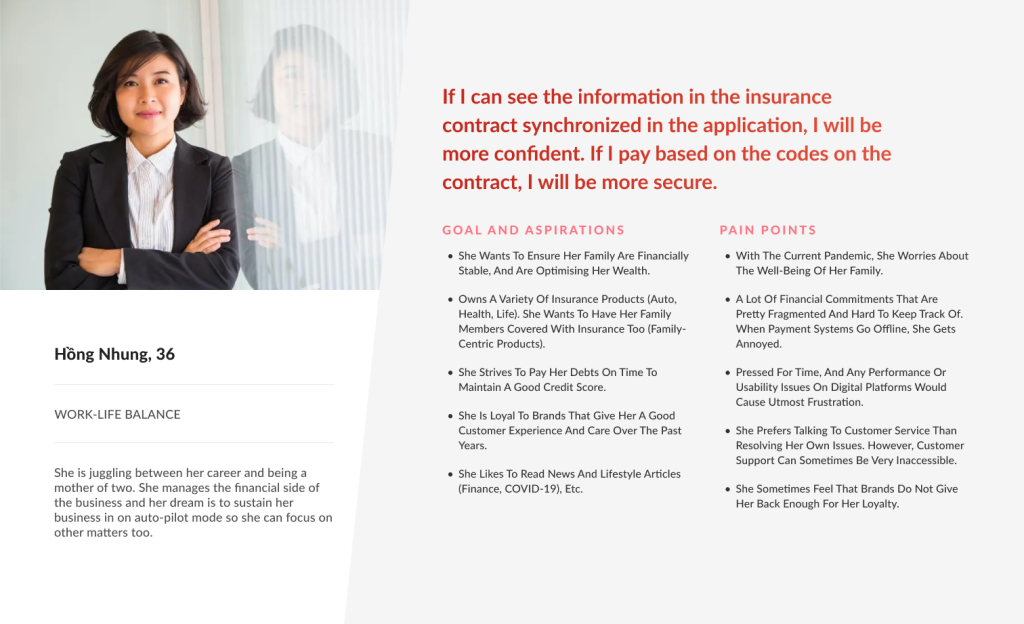

User personas

Based on our desk research, stakeholder interviews and user interviews, we formulated the following user persona framework to help shape our approach to the product’s features.

This framework is widely used in product development across industries, and is best suited for financial companies as their user’s needs would evolve as they go through different phases in life.

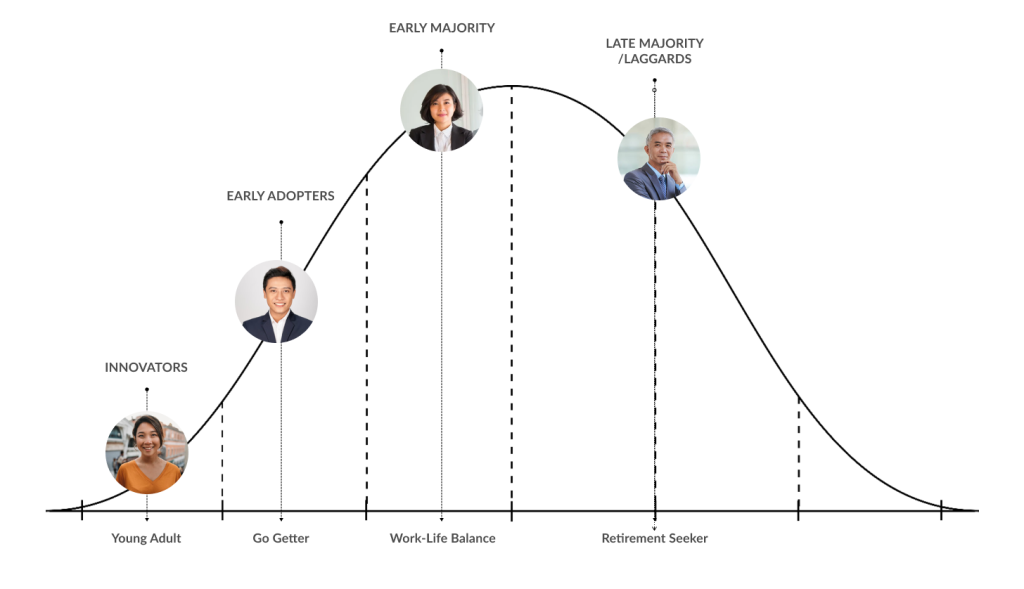

Mapping our personas against the adoption curve, we can easily grasp the tech savviness levels of our user personas.

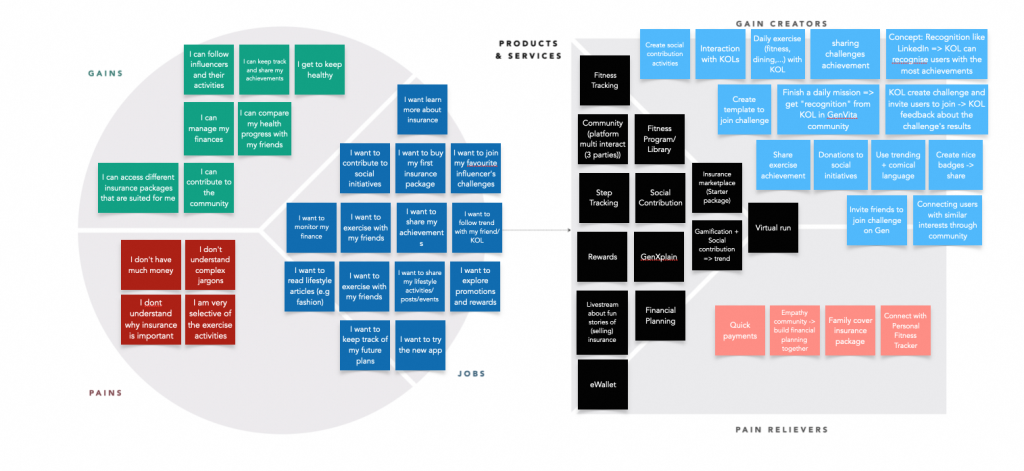

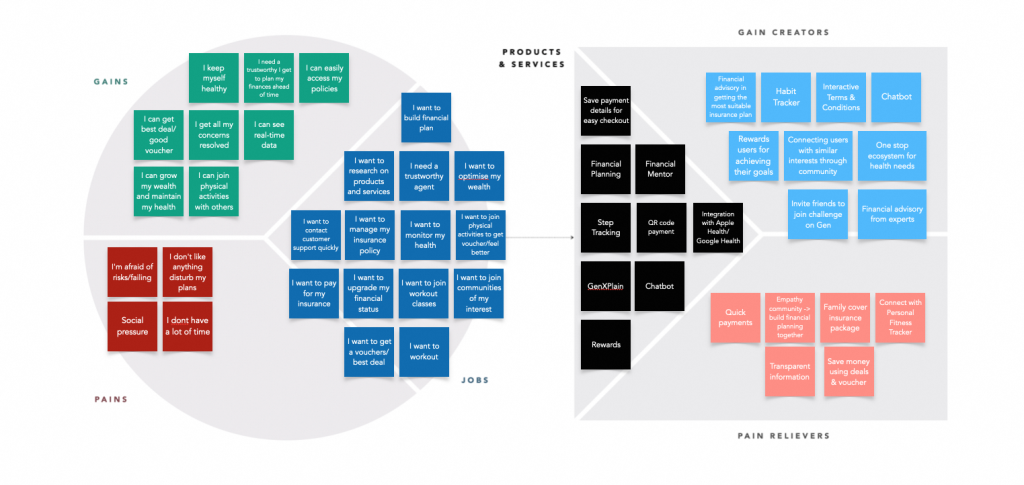

Empathy Mapping

Design Principles

Based on our landscape review, stakeholder interviews, user interviews and brainstorming workshops, I formulated the following principles to help shape our approach to design during the project.

Conversational Tone

Ensuring that our UI and tone is conversational and layman to better cater to not just sophisticated users, but also users that are new to insurance. This could help us expand our reach to the younger audience.

Creating Habits

Implementing habitual features that could drive daily engagement. This ranges from rewarding users for completing a task on the app, to providing basic and complex needs such as insurance and non-insurance services.

Accessible Guidance

Ensuring that our users are able to seek for guidance and support at any stage of their engagement. This can be done by making customer support more accessible, including educational materials to increase literacy, and also providing a digital assistant that can guide users without the need of an agent.

3/ Starting the Design

Applying UX Laws – I reviewed the foundational UX laws – a series of best practices for building user interfaces. Using psychology in design helped shed light on user expectations, improving the overall user experience.

Fitt’s Law

Large buttons placed in the thumb zone ensure users can quickly, easily and accurately access major functions

Hick’s Law

Highlight compulsory fields to avoid overwhelming users, and place optional fields in separate location

Jakob’s Law

Use familiar UI patterns for input fields such as dropdowns, error states, etc to leverage existing mental models

Von Restorff Effect

The distinct Gumtree brand colour (green) guides users through each step of the core task flow

Zeigarnik Effect

Stepper bars at the top provide a clear indication of progress to motivate users to complete tasks

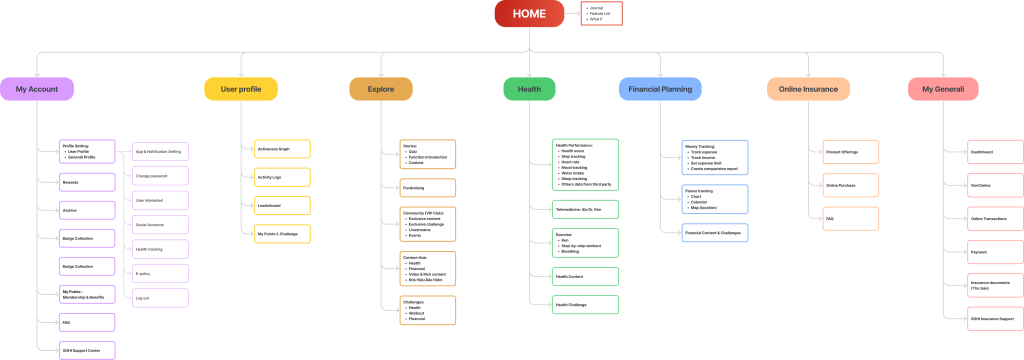

Information architecture

Finalising the design

Due to NDA restriction, I’m unable to show full design of this product.